Loading content...

Articles

India’s Software-Defined Vehicle Platform

India’s Software-Defined Vehicle Platform

How AI Disruption, Unique Road Conditions, and Cross-Segment Volume Economics Converge to Create India's Next Industrial Revolution

India simultaneously confronts three structural crises that, individually, each represents a national emergency. Taken together, they demand a single, integrated industrial response. The Software-Defined Vehicle platform is that response.

India's information technology and business process outsourcing sector generates approximately $254 billion in annual revenue (FY2024, NASSCOM) and directly employs 5.43 million professionals. Including indirect employment in real estate, transport, food services, retail, and ancillary industries that serve IT campuses and their workers, the sector supports an estimated 15-20 million livelihoods. For two decades, IT services has been the backbone of India's current account surplus in services, the primary employer of English-speaking graduates, and the single most important channel through which India's demographic dividend has been converted into productive economic output.

This engine is now breaking. Not gradually, not speculatively, but visibly and rapidly.

The data is unambiguous. TCS, India's largest IT employer, announced its largest-ever layoffs in mid-2025, cutting 12,000 positions (2% of workforce) in FY2025. In Q3 FY2025 (ending September 2025), TCS headcount fell by a further 20,000 due to a combination of voluntary departures and layoffs, with company executives explicitly citing AI-driven 'skill mismatches' as a primary driver. Infosys reduced headcount by approximately 20,000 (7%) between FY2023 and FY2025. Across the Indian IT sector, over 50,000 jobs were cut in 2024 alone, predominantly among entry-level programmers and software testers whose tasks are most susceptible to generative AI automation.

These are not cyclical adjustments. They are structural. An IIM Ahmedabad study of white-collar workers found that while 55% have adopted AI tools and 48% have received AI training, 68% fear their roles could be automated within five years. The World Economic Forum projects that 40% of employers globally will reduce staff where AI can automate tasks. In India's IT sector specifically, estimates suggest 40-50% of current white-collar roles face displacement risk.

The Core Problem: India needs to create approximately 8 million jobs annually to absorb its working-age population growth. If even 20-30% of IT services jobs are displaced (1-1.6 million direct, 3-5 million indirect), the country faces a net employment gap of 4-7 million jobs per year in precisely the demographic that has driven urban consumption growth.

Previous technology transitions (mainframe to client-server, on-premise to cloud) created more Indian IT jobs than they destroyed because they expanded the total addressable market for outsourced services. AI is different for a structural reason: it substitutes for the cognitive labor that is India's core export. When ChatGPT and Claude can write, debug, and test code; when GitHub Copilot autocompletes entire functions; when AI agents can handle L1 customer support in natural language, the task that Indian IT workers perform is the task being automated.

India's major IT companies have compounded this vulnerability by underinvesting in R&D. Over the past five years, India's top IT firms spent approximately 2% of revenue on research and development. By comparison, Microsoft spent $33 billion on R&D in FY2025, equivalent to 12% of its $282 billion revenue, and more than TCS's total $30 billion in revenues. Indian IT has been an arbitrage business, not a technology business, and AI eliminates the arbitrage.

India requires a new employment engine that can absorb millions of skilled workers, pay comparable or higher wages, generate export revenue, and create a sustainable competitive advantage rather than another arbitrage opportunity. The replacement must be in a domain where India has structural advantages that AI cannot easily erode, where physical-world complexity creates defensible moats, and where the domestic market provides sufficient scale to bootstrap global competitiveness.

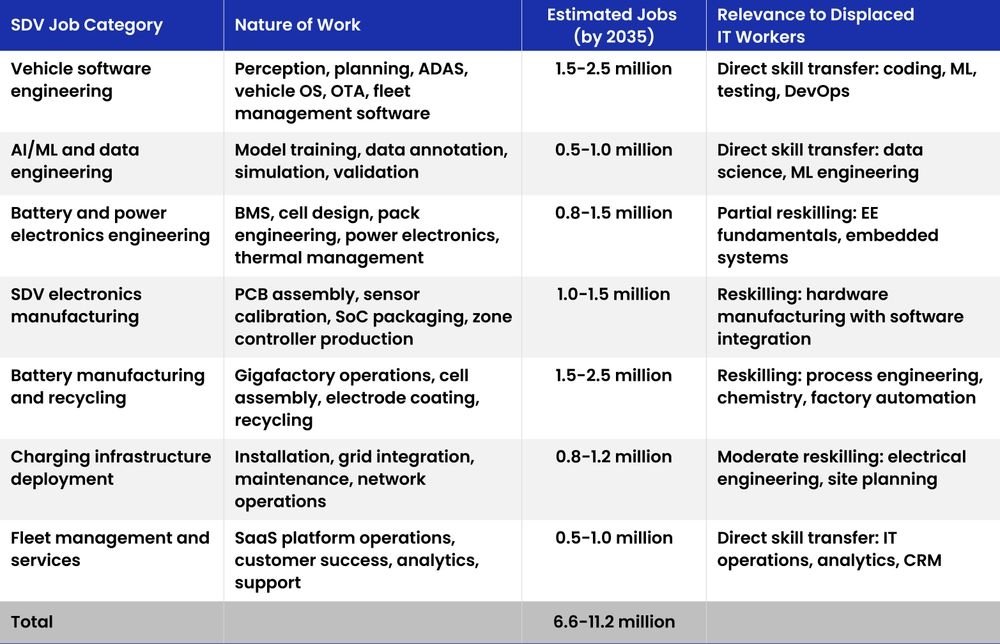

The automotive sector, reimagined through the SDV platform, meets every one of these criteria. It already employs 30-37 million people (4.2 million direct), contributes 6-7.1% of GDP, and generates $240 billion in annual turnover. The SDV transformation converts it from a hardware manufacturing business into a software-hardware integration platform, creating precisely the kind of high-skill jobs that displaced IT workers can transition into.

India imported 232.5 million metric tonnes of crude oil in FY2023-24 at a cost of $132.4 billion. Import dependency has risen to 88.2% (H1 FY2024-25). This single commodity accounts for approximately one-third of India's total merchandise imports and is the largest structural driver of the current account deficit, which stood at 1.0-1.3% of GDP in recent years.

Road transport consumes approximately 70% of all diesel and 99.6% of all petrol sold in India. The transport sector's petroleum consumption represents approximately $55-70 billion of the annual oil import bill. This is the addressable market for transport electrification. Every dollar of oil not imported is a dollar that stays in the Indian economy, pays Indian electricity generators, supports Indian coal miners or solar panel manufacturers, and strengthens the rupee.

The Structural Arithmetic: India's oil import bill ($130-145 billion/year) exceeds its entire IT services export revenue (~$120 billion/year). The country runs a services surplus to finance a petroleum deficit. If AI erodes the services surplus while the petroleum deficit persists, India faces a balance of payments crisis. Transport electrification is the only intervention that addresses both sides of this equation simultaneously.

Every $10/barrel increase in crude oil prices adds approximately $15 billion to India's annual import bill, widens the CAD by 0.4-0.5% of GDP, depreciates the rupee by 2-3%, adds 30-50 basis points to CPI inflation through direct fuel costs and second-order logistics cost pass-through, and forces the RBI into tighter monetary policy that constrains growth. India is a price-taker in global oil markets with zero ability to influence pricing, making the economy structurally hostage to OPEC production decisions, Middle Eastern geopolitics, and global commodity speculation.

Electrification converts this uncontrollable external variable into a controllable domestic one. Grid electricity pricing in India is regulated, domestically sourced, and declining in real terms as renewable energy capacity expands. The SDV platform replaces oil dependency with grid dependency, and India controls its own grid.

India recorded over 177,000 road accident fatalities in 2024, a 2.3% increase over the previous year, equivalent to 485 deaths every day or approximately one death every three minutes. In just the first six months of 2025, 29,018 lives were lost on national highways alone, already exceeding 50% of the full-year 2024 national highway death toll of 53,090. The trajectory is worsening, not improving.

Two-wheeler riders account for nearly half of all road accident deaths. 66% of fatalities are in the 18-34 age group, India's most economically productive demographic. National highways, which constitute just 2% of India's road network by length, account for over 30% of all road accidents and 36% of deaths. The World Bank has estimated the total economic cost of road traffic injuries in India at 3-5% of GDP, encompassing medical costs, lost productivity, property damage, and administrative expenses.

The fundamental problem is human error interacting with vehicle limitations. Over-speeding, distracted driving, fatigue, and poor judgment account for the overwhelming majority of crashes. ADAS technologies, which the SDV platform delivers as standard, directly address these causes. Automatic Emergency Braking (AEB) alone has been shown to reduce rear-end collisions by 40-50% in Western studies. In Indian conditions, where following distances are shorter and hazard density is higher, the potential impact is even greater.

The Human Cost Arithmetic: 180,000 deaths equals an entire mid-sized city eliminated every year. 30,000 were riders without helmets. 10,000 were school students. At 66% in the 18-34 age bracket, India is losing the very demographic cohort it needs to power its economic growth. Each death represents an average of 30-40 lost productive years. The aggregate lost productivity from road deaths alone exceeds $25 billion annually.

The three crises described above, taken together, define both the problem and the solution space. India needs a technology platform that creates millions of high-skill jobs, eliminates oil dependency, and saves lives through vehicle intelligence. The Software-Defined Vehicle platform, specifically designed for India's unique conditions and leveraging India's unique production volume, is that platform. This section explains why India's road conditions create a competitive moat and why India's production volume creates unassailable economics.

Conventional wisdom treats India's chaotic road conditions as a barrier to vehicle intelligence. This analysis inverts that assumption: India's road conditions are not a bug but a feature. They constitute the most complex driving environment on Earth, and any SDV system that works reliably in India will work everywhere else with minimal adaptation. This is India's moat, and it is unreplicable because it is rooted in physical, cultural, and infrastructural conditions that no simulation or synthetic dataset can fully capture.

Heterogeneous Traffic Mix

Indian roads simultaneously carry two-wheelers (scooters and motorcycles), three-wheelers (auto-rickshaws and cargo), passenger cars, SUVs, light commercial vehicles, medium and heavy trucks, buses (city, intercity, school, staff), tractors, bullock carts, cycle rickshaws, hand carts, pedestrians (including children, elderly, and persons carrying head-loads), cyclists, and animals (stray dogs, cattle, buffalo, camels, elephants in certain states). No other country's road network routinely carries this diversity of traffic participants sharing the same carriageway at the same time. A perception system trained to reliably detect, classify, and predict the behaviour of all these road users is over-specified for any other market in the world.

Lane-Less Driving and Negotiated Right of Way

Lane markings in India are largely decorative. Vehicles occupy whatever lateral space is available, creating a fluid, continuously negotiated traffic flow that bears no resemblance to the lane-based driving model assumed by Western ADAS and autonomous driving systems. Right of way at intersections is determined in real-time through a complex social negotiation involving vehicle size (larger vehicles have implicit priority), relative speed, eye contact, horn usage, and collective momentum. This negotiation is unwritten, culturally embedded, and not captured in any traffic rule book. An SDV system that can navigate Indian intersections can navigate any intersection on Earth.

Horn-Based Communication Protocol

Indian drivers communicate intent primarily through horn patterns rather than turn signals or lane position. A single short honk means 'I am here, be aware.' A double honk means 'I am overtaking.' Sustained honking means 'Move aside.' Rhythmic honking from a truck means 'I am heavily loaded and cannot stop quickly.' Flash-to-pass (headlight flashing) means 'I am not yielding; you yield.' These are unofficial but universally understood protocols. An SDV system operating in India must not only perceive visual and radar data but must integrate acoustic signals into its prediction model, a capability unnecessary in most other markets but immensely valuable as an additional sensing modality.

Road Surface Variability

A single journey in India can transition from a world-class six-lane expressway to a potholed state highway to an unpaved village road within 50 kilometres. Speed breakers (speed bumps) are frequently unmarked, inconsistently sized, and sometimes improvised from piled gravel or asphalt. Potholes and open manholes are dynamic obstacles that appear and disappear with monsoon cycles. Road geometry changes without warning: sudden narrowing, unannounced median breaks, missing crash barriers, and construction zones with no signage. An SDV suspension and path-planning system designed for this variability produces a far more robust vehicle than one designed for consistent European or American road surfaces.

Extreme Environmental Conditions

India's climate envelope spans from 52 degrees Celsius in Rajasthan's Thar Desert to minus 40 degrees Celsius in Ladakh. Annual monsoon rainfall can exceed 2,000mm in Mumbai and the Western Ghats, causing urban waterlogging (30-60cm depth on roads), zero-visibility downpours, and hydroplaning. Dust storms in northern India can reduce visibility to under 50 metres and coat sensor surfaces within minutes. Dense fog in the Indo-Gangetic plains (November to February) creates visibility below 20 metres for weeks at a stretch. High-altitude driving above 3,000 metres affects engine performance, battery chemistry, and electronic cooling. Any sensor suite, battery management system, and thermal architecture validated across this envelope is validated for every climate on Earth.

Night Driving Challenges

Roughly 30% of India's road fatalities occur between 6 PM and midnight. Oncoming vehicles frequently drive on high beam, creating glare that blinds human drivers. Pedestrians and cyclists on unlit rural roads wear dark clothing with no reflective elements. Unladen trucks and tractors sometimes drive without tail lights. Overloaded vehicles protrude into adjacent lanes without any marking. These conditions demand perception systems that work in extreme glare, low-contrast, and mixed-illumination scenarios, exactly the conditions that challenge camera-based perception systems most severely, forcing the development of robust multi-modal sensor fusion.

The Training-at-Altitude Analogy: Athletes who train at high altitude develop greater aerobic capacity that gives them an advantage at sea level. The same principle applies to SDV systems. A perception and planning stack trained and validated on Indian roads, with their unmatched complexity, density, and unpredictability, is fundamentally over-specified for any other market. An Indian SDV system deployed in Germany or Japan or Brazil will encounter a strict subset of the scenarios it already handles. This is a permanent, structural advantage rooted in physical reality that cannot be replicated by simulation, synthetic data, or training on simpler road environments.

The competitive implications are profound. Western SDV development (Waymo, Tesla, Cruise, Mobileye) has been optimised for lane-based, signal-regulated, homogeneous-vehicle traffic. These systems struggle with edge cases that are routine in India. Indian SDV development, if done systematically on Indian roads, produces systems that handle the Western driving environment as a trivial subset. India's chaotic roads are not a barrier to SDV deployment; they are the basis for a global technology advantage.

Driving data from Indian roads is the scarcest and most valuable SDV training dataset in the world. No Western company has it at scale. The IIT Hyderabad TiHAN consortium's 4,000-kilometre data collection drive (Hyderabad to Jammu and back, January 2025) represents one of the first systematic efforts to build an Indian driving dataset. The SDV platform, deployed across 2.5 million vehicles generating continuous driving data, would create an unprecedented corpus of real-world Indian driving scenarios that compounds over time and cannot be replicated by any competitor without equivalent fleet deployment in India.

This data has dual value: it trains Indian SDV systems for the domestic market, and it creates a licensable asset for any global OEM seeking to enter India or other similarly complex markets (Southeast Asia, Africa, Latin America, the Middle East). The data moat is a recurring revenue stream, not a one-time advantage.

India manufactures approximately 25 million vehicles annually across six distinct segments: roughly 20 million two-wheelers, 1-1.5 million three-wheelers, 0.6-0.9 million light commercial vehicles, 80,000-120,000 medium-duty trucks, 100,000-150,000 heavy-duty trucks, and 35,000-45,000 buses. No other country produces vehicles across this breadth of segments at this volume in a single national market

The SDV platform's central insight is that the core compute module, the system-on-chip (SoC) with AI inference capability, safety-certified zone controllers, and connectivity hardware, can be architecturally common across all six segments. A two-wheeler scooter and a 49-tonne truck both require the same fundamental capabilities: sensor data processing, actuator control, OTA update capability, fleet connectivity, and safety monitoring. They differ in the number of sensors, the number of actuators, and the power of the AI inference engine, but these are parametric variations on a common hardware and software platform, not fundamentally different architectures.

At single-segment volumes, a vehicle-grade SoC with AI inference capability costs $25-40 per unit. At India's cross-segment volume of 2.5 million units (10% penetration) scaling toward 12+ million units (50% penetration), the same SoC costs $8-12. This is the volume that makes a fully software-defined electric scooter at Rs 1.1 lakh commercially viable, because the electronics module amortised at Rs 12,000 only works when the same silicon goes into trucks and buses too.

The SDV platform splits cleanly between two powertrain architectures, determined by use case physics rather than aspiration or regulation:

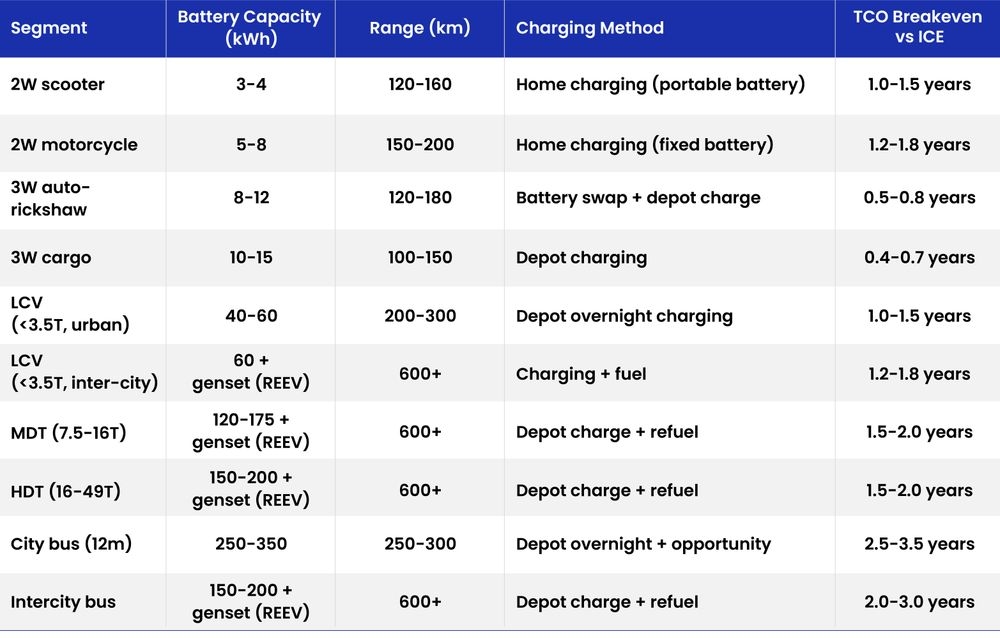

Pure Battery Electric Vehicle (BEV): All two-wheelers, all three-wheelers, sub-1-tonne LCVs, urban 1-3.5 tonne LCVs, city buses (9m and 12m), school buses, and staff buses. The common thread is depot-return or home charging, predictable routes, and daily range under 250 km. These segments can be fully electrified with LMFP batteries at $70-80/kWh pack cost (2027-28 timeline) with zero compromise on operational capability.

Series Hybrid Range-Extended Electric Vehicle (REEV): Inter-city 1-3.5 tonne LCVs, medium-duty trucks (7.5-16 tonnes), heavy-duty trucks (16-49 tonnes), and intercity buses. The physics is unforgiving: a 600 km pure BEV heavy truck requires a 720 kWh battery weighing 4,500 kg, destroying payload economics. The REEV solution uses a 150-200 kWh battery plus a small diesel or CNG genset, saving 3,150 kg of cargo capacity. Critically, the REEV is a series hybrid (genset charges battery, only electric motors drive wheels), never parallel. This preserves full X-by-wire software control and makes the genset a physically removable module. When megawatt charging infrastructure arrives (circa 2030), unbolt the genset, add battery, push a software update. BEV conversion with zero drivetrain changes.

The Critical Architectural Insight: Series hybrid, never parallel. All propulsion stays electric. The genset only charges the battery. This means the entire SDV software stack (traction control, regenerative braking, stability management, ADAS) works identically whether the vehicle is in pure BEV mode or REEV mode. The genset is a 'range anxiety eliminator' that becomes redundant as charging infrastructure matures. This is a 10-year bridge technology with a guaranteed sunset, not a permanent architectural compromise.

This section provides a comprehensive description of every layer of the SDV platform, from silicon to cloud, designed specifically for India's requirements. The stack is described bottom-up, from hardware through software to services, reflecting the dependency chain in which each layer builds on the one below it.

The heart of every SDV vehicle is a central system-on-chip (SoC) providing AI inference, sensor fusion, and vehicle-wide coordination. The platform specifies an ARM-based SoC with 50-200 TOPS (tera operations per second) of AI inference capability, scalable through software configuration: 50 TOPS for two-wheelers (basic ADAS), 100 TOPS for three-wheelers and LCVs (Level 2 ADAS), and 200 TOPS for commercial vehicles (Level 2+ with fleet management). The SoC integrates CPU cores (8-12 ARM Cortex-A series), a neural processing unit (NPU) for AI inference, an image signal processor (ISP) for camera inputs, a safety island (lockstep cores for ASIL-D functional safety), and high-speed I/O for vehicle Ethernet. Target power consumption is 15-45W depending on configuration, enabled by 5nm or 4nm process node fabrication.

India's semiconductor fabrication roadmap (Tata Electronics partnership with PSMC for 28nm, Vedanta's proposed fab) provides a pathway to domestic SoC packaging and, eventually, partial fabrication. Even at the 28nm node, zone controllers and power management ICs can be fabricated domestically, with only the central SoC requiring advanced-node imports from TSMC or Samsung foundries.

The platform adopts a camera-first, radar-augmented sensor architecture. No LiDAR. This is a deliberate design choice driven by India-specific economics and conditions.

The decision to exclude LiDAR is driven by three factors. First, cost: LiDAR adds $500-2,000 per vehicle, which is unacceptable for a scooter selling at Rs 1.1 lakh or an auto-rickshaw at Rs 3 lakh. Second, durability: spinning LiDAR units have mechanical components that degrade rapidly in India's dust and vibration environment. Third, diminishing returns: in India's dense, slow-speed traffic (urban speeds of 20-40 km/h), camera+radar provides sufficient perception at a fraction of the cost. The SDV platform's acoustic sensing integration (microphone arrays for horn detection) provides an additional sensing modality that partially compensates for LiDAR's absence while adding a capability LiDAR-equipped Western vehicles lack.

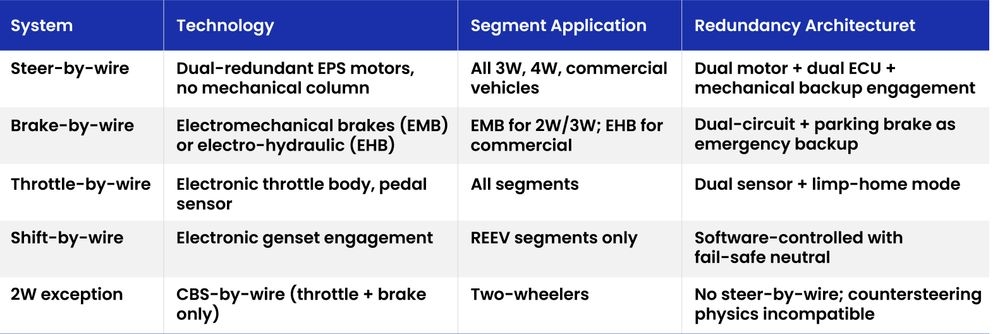

X-by-wire replaces mechanical linkages (steering column, brake cables, throttle cable) with electronic control, enabling the SDV software stack to directly command all vehicle dynamics. This is the single most important architectural decision in the platform, because without X-by-wire, the SDV is merely an instrumented vehicle. With X-by-wire, the software becomes the vehicle.

The two-wheeler exception deserves emphasis. Motorcycle steering involves countersteering (pushing the handlebar in the opposite direction of the intended turn), lean-angle dynamics, and continuous gyroscopic feedback that riders process subconsciously. Steer-by-wire for motorcycles would require recreating this entire haptic feedback loop electronically, which is 5-10 years premature in terms of both technology readiness and rider acceptance. However, two-wheelers get throttle-by-wire (enabling traction control and lean-angle-sensitive ABS) and brake-by-wire (enabling combined braking system by wire, or CBS-by-wire), which together deliver the most safety-critical ADAS functions: automatic emergency braking, traction control, and lean-angle ABS. These three features alone could prevent an estimated 15-25% of the 85,000+ annual two-wheeler fatalities in India.

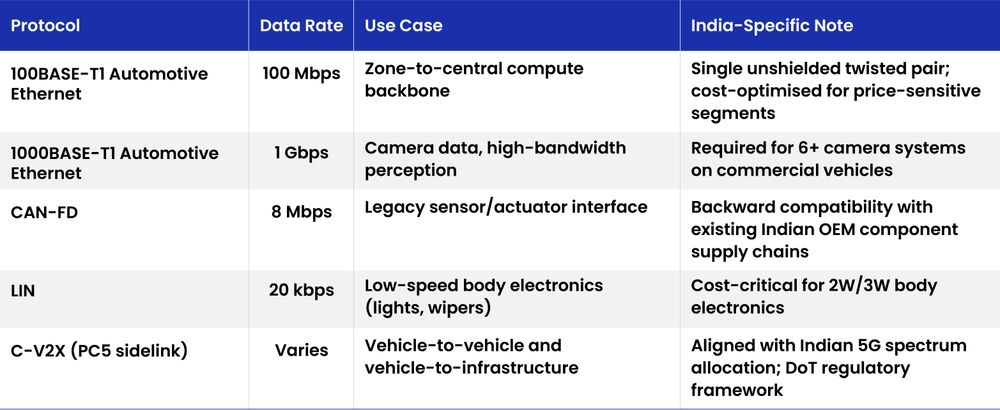

Traditional vehicle electrical architecture uses domain-based ECUs: one for powertrain, one for chassis, one for body, one for infotainment. This creates a wiring harness of 40-100 kg containing 1,500-3,000 individual wires, each running from a sensor or actuator to its dedicated ECU. The SDV platform replaces this with a zonal architecture: the vehicle is divided into 4-6 physical zones (front-left, front-right, rear-left, rear-right, centre, optional roof), each served by a zone controller that aggregates all sensor and actuator signals within its zone and communicates with the central compute module over a high-speed vehicle Ethernet backbone.

Benefits are substantial. Wiring harness weight reduces by 30-40% (saving 12-40 kg depending on vehicle size), which directly improves BEV range. Assembly labour for the harness drops by 25-35%. Most importantly, the zonal architecture creates a clean abstraction layer: the central compute sees standardised data streams from each zone, regardless of the specific sensors and actuators installed. This enables hardware-software decoupling, the foundational principle that makes the vehicle 'software-defined' rather than 'hardware-determined'.

The SDV platform uses a dual-partition (A/B) update architecture with delta compression, enabling the vehicle software to be updated without physically visiting a service centre. Partition A runs the current software while Partition B receives the update. On successful validation, the system boots from Partition B. If the update fails, automatic rollback to Partition A ensures the vehicle remains operational.

India-specific OTA considerations include bandwidth awareness (updates must work over 4G/LTE connections with 2-10 Mbps throughput, not just 5G), download scheduling (overnight when vehicles are parked and on WiFi or stable cellular), resumable downloads (to handle India's intermittent connectivity), and regional staging (update servers must be distributed across Indian CDN nodes, not dependent on international bandwidth). The platform targets a maximum OTA update size of 500 MB (compressed) for a full system update, achievable within 30-60 minutes even on 4G.

The software stack is the layer that makes the vehicle 'software-defined.' It is where the majority of the platform's value resides, where the majority of new jobs are created, and where India's competitive advantage is most defensible. The stack comprises four sub-layers: the real-time operating system, the vehicle operating system, the middleware and services framework, and the application layer.

Safety-critical functions (brake control, steering control, battery management, motor control) execute on zone controllers running a deterministic real-time operating system certified to ISO 26262 ASIL-D, the highest automotive safety integrity level. These functions have hard real-time requirements: a brake command must be executed within 10 milliseconds, with guaranteed worst-case execution time regardless of system load. The RTOS layer is the smallest, simplest, and most rigorously validated layer of the stack. It changes rarely (annual updates at most) and is subject to formal verification methods.

The central compute module runs a Linux-based vehicle operating system with an AUTOSAR Adaptive middleware layer. A Type-1 hypervisor enables mixed-criticality execution: safety-critical functions (ASIL-B rated) run in an isolated partition alongside the general-purpose Linux partition that runs perception, planning, connectivity, and infotainment. This architecture allows the AI/ML perception stack to be updated frequently (monthly or even weekly via OTA) without re-certifying the safety-critical partition.

India localisation requirements for the vehicle OS include multi-language HMI support (22 official languages under the Eighth Schedule, with at minimum Hindi, English, Tamil, Telugu, Marathi, Bengali, Gujarati, and Kannada at launch), regional voice command recognition (Indian-accented English plus vernacular languages), and compliance with Indian data localisation regulations (AIS-189 and emerging DPDPA requirements for vehicle data residency).

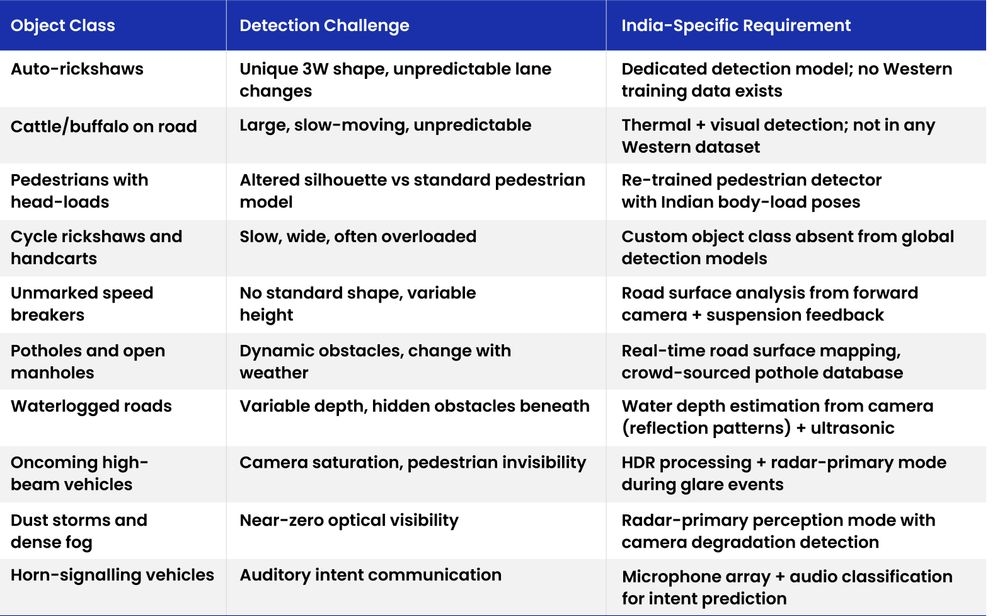

This is the layer where India's road conditions create the competitive moat. The perception system must detect, classify, track, and predict the behaviour of every object class in the Indian traffic taxonomy:

Each of these object classes requires India-specific training data that does not exist in any Western driving dataset (nuScenes, Waymo Open, KITTI, Argoverse). The SDV platform's fleet deployment generates this data at scale: 2.5 million vehicles, each generating continuous driving data, creates a dataset that compounds with every kilometre driven. This is the data moat that makes the Indian SDV platform globally unique.

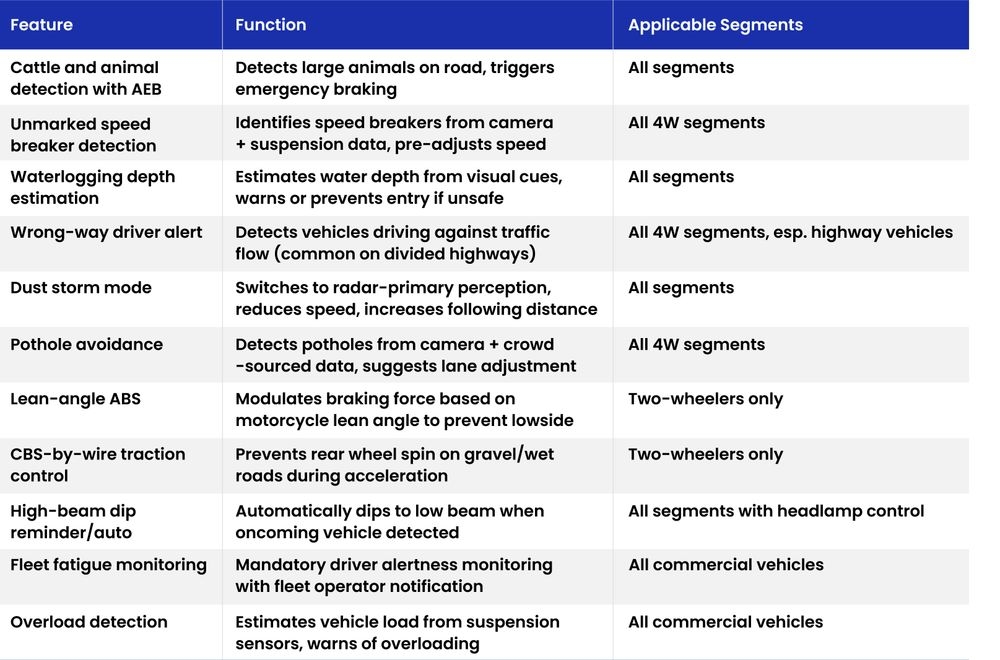

Beyond the standard ADAS feature set (AEB, ACC, LKA, BSD, RCTA), the SDV platform includes features designed specifically for Indian conditions:

The SDV platform's software-defined nature enables a post-sale revenue model through application updates and services. Unlike a traditional vehicle where features are fixed at the factory, the SDV can receive new capabilities via OTA throughout its lifetime. This creates a software-as-a-service layer analogous to the smartphone app ecosystem:

Feature upgrades (paid OTA): Enhanced ADAS modes, performance tuning (motor torque curves), range optimisation algorithms, new voice assistant capabilities. Insurance integration: Real-time driving behaviour scoring fed to insurance providers for usage-based insurance (UBI) pricing, reducing premiums for safe drivers by 20-40%. Fleet management: Route optimisation, driver performance scoring, fuel/energy consumption analytics, predictive maintenance scheduling, regulatory compliance documentation (e-way bills, driver hours). Energy management: Smart charging optimisation (charge when electricity is cheapest), vehicle-to-grid (V2G) discharge during peak demand for revenue, fleet-wide charge scheduling to avoid grid stress. Predictive maintenance: AI-based prediction of component wear (brake pads, tyre tread, battery degradation) enabling scheduled rather than breakdown maintenance, critical for commercial fleet uptime.

The platform standardises on lithium manganese iron phosphate (LMFP) battery chemistry across all segments. LMFP is the evolutionary successor to LFP (lithium iron phosphate), adding manganese to increase energy density by 15-20% while retaining LFP's core advantages: no cobalt or nickel dependency (both conflict minerals with volatile pricing), thermal stability (no thermal runaway risk, critical for Indian temperatures), cycle life exceeding 3,000 cycles (10+ years at daily use), and projected pack cost of $70-80/kWh by 2027-28.

For India, LMFP's advantages over NMC (nickel manganese cobalt) chemistries are decisive. NMC requires active thermal management to prevent thermal runaway above 40 degrees Celsius. In Indian summers, this means continuous cooling energy consumption, reducing effective range by 10-15%. LMFP's thermal stability window extends to 60 degrees Celsius with minimal derating, making it inherently suited to Indian climate without the energy penalty of aggressive cooling. The platform's battery-agnostic BMS architecture also supports future chemistry migration to sodium-ion (for ultra-low-cost 2W/3W) or solid-state (when commercially available post-2030) without hardware redesign.

The platform uses permanent magnet synchronous motors (PMSM) with silicon carbide (SiC) inverters for all segments above 2W. Two-wheelers use BLDC (brushless DC) motors with IGBT inverters for cost optimisation. PMSM motors offer 92-96% efficiency across the operating range, and SiC inverters reduce switching losses by 30-50% compared to silicon IGBTs, directly translating to extended range. Motor sizes range from 5 kW (scooter) to 350 kW (heavy truck, dual motor). Regenerative braking recovers 15-25% of energy depending on route profile, with Indian urban stop-start traffic delivering higher recovery rates than highway driving.

For REEV segments, the range-extending genset is a compact, constant-speed engine-generator unit. Because it operates only at its optimal efficiency point (charging the battery at a fixed RPM), it achieves 35-40% thermal efficiency versus 25-30% for a conventional variable-speed diesel engine driving through a transmission. The genset is specified as a 50-120 kW diesel or CNG unit depending on vehicle class, mounted as a bolted module with standardised electrical and cooling connections. The modular design means the genset can be physically removed and replaced with additional battery modules when megawatt-class charging infrastructure makes pure BEV operation practical for long-haul routes, estimated to be feasible by 2030-2032.

Every SDV vehicle includes a cellular connectivity module (4G/LTE at launch, 5G-ready) with embedded SIM. This provides continuous cloud connectivity for OTA updates, real-time fleet management, V2X communication, emergency call (eCall, required by AIS-140 for commercial vehicles), and data upload (driving data, diagnostic data, anonymised traffic data). The connectivity module supports India's NavIC (IRNSS) satellite navigation system alongside GPS and GLONASS for positioning accuracy, and the Unified Payments Interface (UPI) for in-vehicle payment integration (toll collection, charging payment, parking).

The SDV cloud platform serves four functions. First, data ingestion and storage: receiving driving data from the fleet for model training, quality analysis, and predictive analytics. Second, AI model training: using fleet-collected data to continuously improve perception, planning, and prediction models, then deploying improved models back to vehicles via OTA. Third, fleet management: providing fleet operators with real-time dashboards for vehicle tracking, driver behaviour scoring, energy consumption analysis, maintenance scheduling, and regulatory compliance. Fourth, digital twin: maintaining a virtual replica of each vehicle's software and hardware state for remote diagnostics, OTA testing, and lifecycle management.

India-specific cloud requirements include data localisation (all vehicle data stored on Indian servers per DPDPA requirements), multi-region deployment (AWS Mumbai, Azure Pune, or domestic cloud providers to ensure low-latency connectivity across India's geography), and bandwidth-optimised data upload (edge processing on-vehicle to reduce upload volume by 90-95%, transmitting only annotated events rather than raw sensor streams).

The SDV Platform Flywheel: More vehicles deployed means more driving data collected. More driving data means better AI models. Better AI models mean safer vehicles and better ADAS features. Better features attract more vehicle buyers and fleet operators. More vehicles deployed restarts the cycle. Simultaneously, better data enables higher-value services (insurance, fleet management, predictive maintenance), generating recurring software revenue that funds further R&D. This is a flywheel with compounding returns, and India's 25 million vehicle annual production provides the initial momentum that no other market can match.

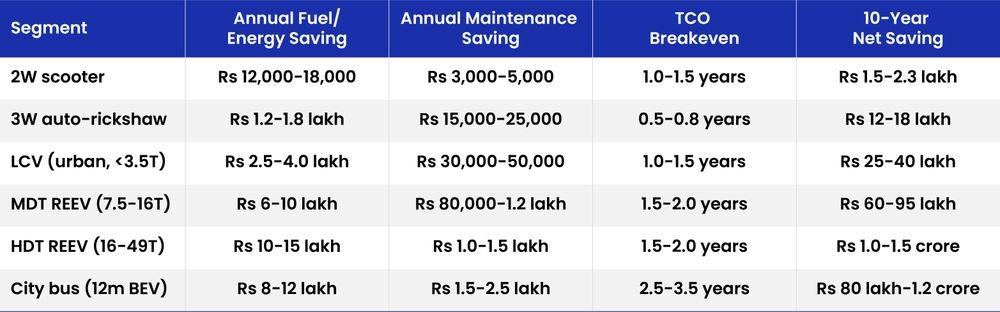

The SDV platform's economic case rests on total cost of ownership (TCO), not purchase price. Electric vehicles have higher upfront cost but dramatically lower operating cost due to three factors: electricity is 70-85% cheaper than diesel/petrol per kilometre; electric drivetrains have 60% fewer moving parts, reducing maintenance cost by 40-60%; and regenerative braking extends brake component life by 2-3x. For commercial vehicles, these savings compound over high annual mileage, creating TCO breakeven in months rather than years.

For fleet operators (trucking companies, bus operators, last-mile delivery firms), the SDV platform's benefits extend beyond fuel savings. Fleet management software integrated into the vehicle reduces deadheading (empty return trips) by 15-25% through route optimisation. Driver behaviour monitoring reduces insurance claims by 20-30%. Predictive maintenance reduces unplanned downtime by 40-60%, critical in commercial transport where a single day of vehicle downtime costs Rs 15,000-50,000 in lost revenue. Over-the-air feature upgrades keep fleet vehicles current without depot visits, reducing service-related downtime by 30-40%.

The combined effect is a 25-40% improvement in fleet operating margin, enough to finance the higher upfront cost of SDV vehicles entirely from operational savings within 1-3 years. For a fleet operator running 100 heavy trucks, this translates to Rs 10-15 crore in annual savings, fundamentally altering the economics of Indian road freight.

The SDV platform enables usage-based insurance (UBI) by providing insurers with real-time driving behaviour data (speed, braking patterns, cornering forces, time of day, route risk profile). This replaces the current actuarial model based on vehicle age, owner demographics, and region with a per-driver, per-trip risk assessment. Safe drivers see premium reductions of 20-40%. Riskier drivers are priced accurately rather than cross-subsidised. The net effect is lower average premiums (because SDV vehicles are inherently safer, with ADAS reducing accident frequency) and more profitable underwriting (because risk pricing is more accurate). For the insurance industry, this is a Rs 15,000-25,000 crore revenue opportunity in new telematics-based products.

Traditional Indian OEMs earn 6-10% EBITDA margins on hardware-centric vehicles. The SDV platform introduces recurring software revenue (OTA feature upgrades, fleet management subscriptions, data licensing) that carries 60-80% gross margins. A vehicle generating Rs 5,000-15,000 per year in software revenue over a 10-year lifetime adds Rs 50,000-1,50,000 in lifetime value per vehicle, equivalent to adding 3-8 percentage points to effective EBITDA margin. At India's production volume, this transforms the automotive industry from a low-margin manufacturing business into a high-margin hardware-plus-software platform.

This is the central economic argument of this document. India's IT services sector faces structural AI displacement of 1-2 million direct jobs and 3-5 million indirect jobs over the next 5-10 years. The SDV platform creates a replacement employment engine that is not only comparable in scale but superior in defensibility, because it is rooted in physical-world complexity rather than cognitive labour arbitrage.

The skill transfer pathway from IT services to SDV is remarkably natural. A Java developer writing enterprise applications can, with 3-6 months of automotive domain training, write AUTOSAR-compliant vehicle software. A data scientist building recommendation engines can be retrained to build perception models for ADAS. A QA engineer testing web applications can test vehicle software with additional safety-critical testing methodology training. A DevOps engineer managing cloud deployments can manage OTA infrastructure. The SDV platform does not require India to build an entirely new workforce; it requires redirecting the existing IT workforce toward a domain where India has physical-world advantages that AI cannot easily automate away.

The Defensibility Argument: AI can automate code writing because code is purely digital. AI cannot easily automate the physical-world complexity of Indian road perception because it requires continuous real-world data collection, hardware-software integration, manufacturing quality control, and local regulatory compliance. The SDV platform creates jobs at the intersection of software and the physical world, exactly where human labour retains maximum value in an AI-automated economy.

At full deployment (approximately 50% of new vehicle sales by 2035), the SDV platform's electrification generates estimated annual oil import savings of $40-55 billion, representing a 30-40% reduction in India's petroleum import bill. Combined with $14-23 billion in additional vehicle and component exports (the platform's India-designed SDV vehicles are globally competitive for price-sensitive markets in Africa, Southeast Asia, Latin America, and the Middle East), the net current account improvement is 0.5-1.3 percentage points of GDP, sufficient to move India from a persistent current account deficit to near balance or even surplus.

This has cascading second-order effects. Reduced oil imports decrease dollar demand, supporting rupee stability and reducing imported inflation. A structurally lower current account deficit improves India's sovereign credit profile, currently at the lowest investment grade (Baa3/BBB-), potentially enabling a ratings upgrade that would reduce government and corporate borrowing costs by 50-100 basis points across the yield curve.

The SDV platform contributes to GDP growth through five channels: direct manufacturing value addition ($25-40 billion annually from SDV vehicle and component production), software and services revenue ($10-20 billion from fleet management, OTA services, data licensing), infrastructure investment ($30-50 billion cumulative in charging networks, battery factories, semiconductor packaging), productivity gains (logistics cost reduction from 8% to 6-7% of GDP through fleet efficiency, route optimisation, and reduced fuel cost, releasing $20-40 billion annually into the productive economy), and health cost avoidance ($15-25 billion annually from reduced air pollution and road accident injuries). The net annual GDP growth addition at steady state is estimated at 0.3-0.5 percentage points, compounding over time.

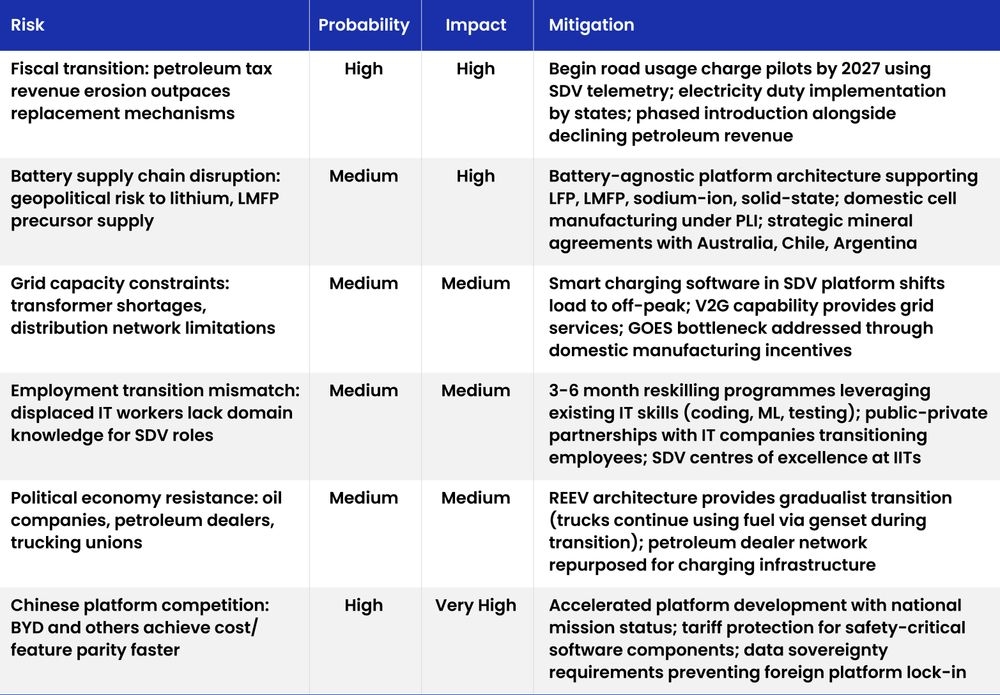

The fiscal transition is the most complex dimension. India's central and state governments collectively collect approximately Rs 7.5 lakh crore ($90 billion) annually from petroleum taxes. As transport electrifies, this revenue stream erodes. However, the SDV platform provides unique mechanisms for revenue replacement that non-SDV electric vehicles cannot: GPS/OBD-based road usage charges (the SDV's always-connected compute module with precise positioning enables per-kilometre, per-axle, per-route tolling that is impossible with conventional vehicles); electricity duty on EV charging (state levy of Rs 1.5-2.5/kWh on commercial charging); battery lifecycle levies; and carbon tax on REEV fuel consumption. The SDV's built-in telemetry makes tax collection enforceable, automatic, and fraud-resistant, unlike manual toll collection or fuel taxation that is susceptible to adulteration and evasion.

India's logistics cost was assessed at 7.97% of GDP (Rs 24.01 lakh crore, approximately $268 billion) in FY2023-24, according to the DPIIT-NCAER study. Road freight remains the most expensive transport mode at Rs 3.78 per tonne-kilometre. The SDV platform reduces logistics cost through four mechanisms: fuel cost reduction (electricity at Rs 7-8/kWh vs diesel at Rs 90/litre translates to 60-70% lower energy cost per tonne-km); fleet efficiency (route optimisation, reduced deadheading, better load matching reduces empty running by 15-25%); reduced downtime (predictive maintenance and OTA updates keep vehicles operational 10-15% more days per year); and driver productivity (ADAS reduces fatigue-related slowdowns and enables longer safe driving hours). The combined effect could reduce logistics cost by 1.5-2.5 percentage points of GDP, equivalent to releasing Rs 4.5-7.5 lakh crore ($50-85 billion) annually into the productive economy.

Vehicular emissions contribute approximately 27% of India's urban PM2.5 pollution. Air pollution is responsible for an estimated 1.67 million deaths annually (Lancet, GBD 2019), with economic costs estimated at 1.36% of GDP in lost output alone. The SDV platform's electrification eliminates tailpipe emissions at the point of use. Even REEV segments operate in zero-emission mode within cities (battery-only mode with geofenced genset lockout). At 50% fleet electrification, the platform reduces vehicular PM2.5 emissions by 30-40%, generating estimated health cost savings of $15-25 billion annually and preventing approximately 40,000-70,000 premature deaths per year.

Road accident reduction through ADAS adds further health economics benefit. If SDV-equipped vehicles reduce involvement in fatal accidents by 25-40% (conservative estimate based on Western AEB effectiveness studies, likely understating India-specific potential given higher hazard density), the platform prevents 15,000-30,000 deaths annually and avoids an estimated $5-10 billion in medical, legal, and lost-productivity costs.

Five forces are converging simultaneously in 2025-2028, creating a window of opportunity that did not exist five years ago and may not remain open indefinitely:

AI threatening IT jobs NOW. TCS's 12,000-person layoff, Infosys's 20,000 headcount reduction, and the broader industry pattern of flat-to-declining hiring make the employment substitution argument urgent rather than theoretical. The displaced workforce is available for redeployment today.

Battery costs hitting economic parity NOW. LMFP pack costs at $70-80/kWh (expected by 2027-28) make BEV scooters, auto-rickshaws, and urban LCVs cheaper than ICE equivalents on both purchase price and TCO. This is the tipping point at which electrification becomes demand-pull rather than subsidy-push.

India's industrial policy aligned NOW. The Production Linked Incentive (PLI) scheme for automotive, batteries, and semiconductors; the PM E-DRIVE scheme for electric vehicle adoption; the National Logistics Policy; and the upcoming National EV Policy collectively create a supportive policy environment worth Rs 50,000+ crore in incentives.

Semiconductor ecosystem emerging NOW. Tata Electronics' fab in Dholera (Gujarat), Micron's assembly and test facility in Sanand, and the growing OSAT (outsourced semiconductor assembly and test) ecosystem provide the beginnings of domestic silicon supply for automotive-grade components.

5G rollout enabling V2X NOW. India's 5G coverage is expanding rapidly, with Jio and Airtel deploying across major urban centres and highways. 5G enables C-V2X (cellular vehicle-to-everything) communication that is foundational for cooperative ADAS and fleet connectivity.

The Window Risk: China's BYD, NIO, and other manufacturers are aggressively expanding into India's SDV market. If India does not build its own SDV platform, it will import one, converting the automotive sector from a domestic manufacturing strength into a foreign technology dependency. The window for indigenous platform development is approximately 3-5 years before Chinese platforms achieve cost and feature parity that Indian OEMs cannot match without a coordinated national effort.

India's Software-Defined Vehicle platform is not an automotive technology project with economic side effects. It is an integrated response to three simultaneous national crises, employment displacement from AI, structural oil import dependency, and a road safety emergency, that happens to be delivered through the automotive sector.

The logic chain is complete and self-reinforcing. AI displaces IT services jobs. The SDV platform creates replacement jobs in vehicle software, AI/ML, battery engineering, and fleet services, domains where physical-world complexity creates defensibility against further AI automation. India's uniquely complex road conditions make Indian SDV systems over-specified for global markets, creating an export advantage. India's uniquely concentrated multi-segment vehicle production (25 million units annually across 2W to HDT) provides platform economics that no other country can match. The resulting electrification eliminates $40-55 billion in annual oil imports, reduces 180,000 road deaths toward the 2030 halving target, and cuts logistics costs by 1.5-2.5 percentage points of GDP.

The numbers are compelling. 6-11 million new jobs replacing 4-7 million at risk. $40-55 billion in annual oil import savings. $15-25 billion in health cost avoidance. $14-23 billion in new exports. 15,000-30,000 lives saved per year through ADAS. A structural current account improvement of 0.5-1.3 percentage points of GDP. And a technology platform with compounding data advantages that grow more defensible with every kilometre driven on Indian roads.

India's unique combination of concentrated multi-segment production volume, growing domestic market, cost-competitive manufacturing, complex driving environment (the world's hardest SDV test case), large skilled software workforce (currently threatened by AI but redirectable to SDV), and supportive policy momentum creates a convergence of conditions that no other economy possesses. The question is not whether India should build this platform. The question is whether India will seize the 3-5 year window before Chinese competitors establish platform dominance in the Indian market.

For policymakers, the implication is clear: the SDV platform warrants treatment as national infrastructure, comparable in strategic importance to the railway network, the national highway programme, or the digital payments stack (UPI), with corresponding institutional support, funding, and regulatory facilitation. For industry, the implication is that Indian OEMs who build on this platform will capture a disproportionate share of the $7-8 trillion Indian GDP in 2035. For investors, this is a multi-decade compounding opportunity at the intersection of electrification, software, AI, and India's demographic dividend.

The convergence is real. The window is open. The arithmetic is overwhelming. The time to act is now.

All rights reserved ©2026 Decimal Point Analytics Pvt. Ltd.