Loading content...

Articles

The Forgotten Gold Vault: India's Role as an IMF Gold Depository

The Forgotten Gold Vault: India's Role as an IMF Gold Depository

Research compiled from IMF Annual Reports, archival documents, and specialist analysis

In a nondescript building in Nagpur, a city at the geographical heart of India, lies one of the world's most overlooked international financial assets, gold held on behalf of the International Monetary Fund. While the Federal Reserve Bank of New York, the Bank of England, and the Banque de France are well-known custodians of IMF gold, few are aware that India has been the fourth designated gold depository since the IMF's founding in 1946.

This article traces the fascinating journey of IMF gold in India, from its initial deposit in Bombay in 1947, through its military-supervised transfer to a secure inland vault in 1956, its growth to over 144 tonnes by the 1970s, and the intriguing question of what happened to it in the 2009-2010 gold sales.

When the IMF was established at Bretton Woods in 1944 and began operations in 1946, its founding charter designated five gold depositories, New York, London, Shanghai, Paris, and Bombay. These locations were chosen because they represented the five countries with the largest IMF quotas at the time.

India's inclusion was not originally planned. The Soviet Union, which had participated in the Bretton Woods conference, was initially expected to hold a top-five quota. When the USSR declined to join the IMF in late 1946, India moved into the fifth position. Early IMF drafts had actually included Moscow on the depository list alongside New York, London, Shanghai, and Paris.

Shanghai, notably, never received any IMF gold. Due to political instability in China, it was "temporarily" removed from the depository list in 1949, a status that technically remains in effect, with China retaining the theoretical right to request reinstatement.

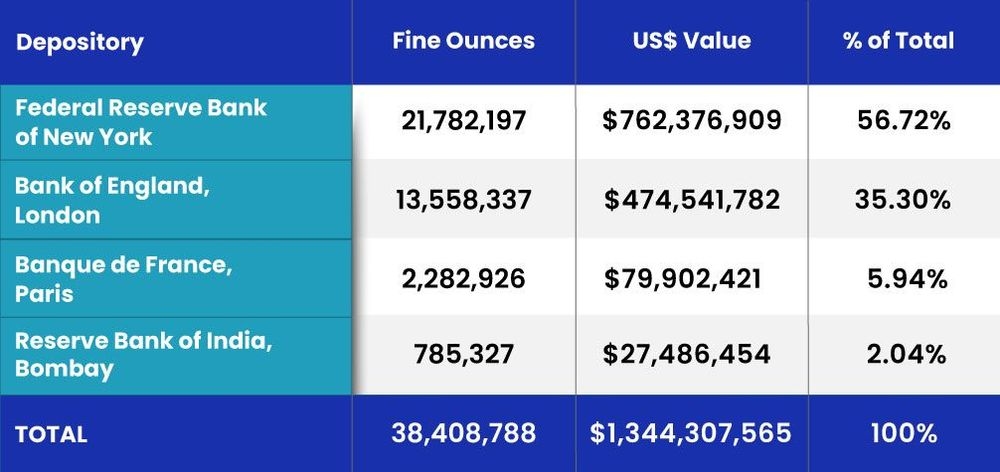

The IMF's first Annual Report (1947) provides the most detailed breakdown of gold holdings by depository ever published. Schedule IV of the Condensed Balance Sheet, dated June 30, 1947, reveals the following distribution:

Source: IMF Annual Report 1947, Appendix VI, Schedule IV

A critical detail, the gold held in Bombay represented solely India's own gold subscription to the IMF. No other member country deposited gold at the Reserve Bank of India. This would remain true throughout the IMF's history, making the India depository unique among the four locations.

In 1956, the Reserve Bank of India made an unusual request to the IMF. The RBI had constructed a new vault at its office in Nagpur, located approximately 520 miles (840 km) inland from Bombay, and wished to transfer both its own gold reserves and the IMF's gold to this more secure location.

The IMF staff document explaining the move stated that the Nagpur vault was built "partly to enable gold to be stored at a comparatively safer place" and partly to relieve pressure on vault accommodation in Bombay.

The transfer arrangements were notable for their security protocols: "The arrangements for transport would be made under the supervision of the military, and safe custody arrangements at Nagpur would be subject to the same security conditions as are observed at present in Bombay."

This transfer had broader implications. The IMF used the occasion to amend its rules (Rule E-1, later Rule F-1), changing the language from specific cities to countries. This gave the Fund flexibility to store gold at any agreed location within the designated countries, a provision that theoretically allows IMF gold to be held at Fort Knox or other US Treasury facilities.

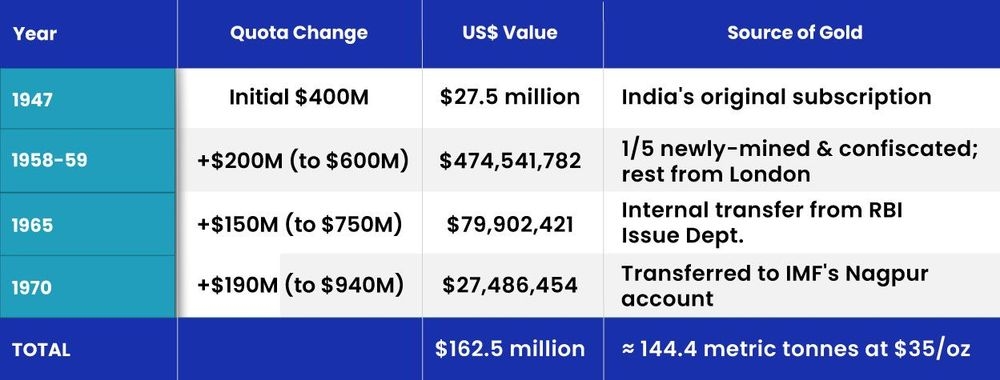

Unlike the other IMF depositories, which received gold from multiple member countries, the Nagpur vault grew only through India's successive quota increases:

This 144.4-tonne figure is verified by the January 1976 IMF monthly financial report, which valued the Reserve Bank of India holdings at SDR 162,499,440, equivalent to approximately 4.64 million ounces.

The quality of IMF gold varies significantly by depository. In New York and Paris, the gold consists primarily of US Assay Office "melts" (batches of 18-22 bars stored as single units) with fineness of 0.995 or better. In London, much of the IMF gold comprises Rand Refinery bars from South Africa, standard good delivery bars.

The Nagpur gold, by contrast, was of variable quality. It included confiscated smuggled gold, newly-mined gold from indigenous Indian production, good delivery bars purchased via the Bank of England, and other gold from the RBI's Issue Department. This heterogeneous composition makes the Nagpur holdings unique in the IMF's portfolio.

The January 1976 IMF financial report provides the last detailed breakdown of gold by depository:

By this point, India's share had more than doubled from its initial 2.04% to approximately 5% of IMF gold holdings.

Here is where the trail grows murky. The IMF no longer publishes depository-level breakdowns of its gold holdings. We know that during the late 1970s gold restitutions, India received back some gold from the IMF into its Nagpur account (members took delivery at the depository in their territory).

The most significant event was the 2009-2010 IMF gold sales, when the Fund sold 403 tonnes of gold:

The IMF never disclosed which depository the sold gold came from. However, analysts have speculated that the sales to India, Bangladesh, Sri Lanka, and Mauritius, all regionally proximate to India, may have been executed by transferring gold from the IMF's Nagpur holding.

If true, this would have effectively "zeroed out" the IMF's Nagpur position, leaving IMF gold in only three countries: the United States, United Kingdom, and France. The variable quality of the Nagpur gold (some of which was non-good-delivery) would make regional sales to neighboring central banks a logical disposition.

Historical Precedent Matters:

India's position as an IMF gold depository dates to the Fund's founding and was shaped by geopolitical accidents (the USSR's non-participation). Understanding these origins provides context for current international monetary arrangements.

Transparency Has Declined:

The IMF's reporting on gold holdings has become less detailed over time. The 1947 annual report provides bar-level precision; today, even country-level breakdowns are unavailable.

Gold Quality Varies:

Not all official gold is created equal. The variable-quality gold in Nagpur (including confiscated and indigenous production) differs markedly from the standardized good delivery bars in London or New York.

Location Flexibility:

The 1956 rule change allowing IMF gold to be stored anywhere within designated countries (not just specific cities) has broad implications, technically allowing gold storage at Fort Knox or other non-traditional locations.

The story of IMF gold in India encapsulates broader themes in international monetary history: the post-war construction of the Bretton Woods system, the evolution of gold's role in international finance, and the increasing opacity of official gold holdings in the modern era.

Whether the Nagpur vault still holds IMF gold remains unknown. The IMF has not confirmed its disposition. What we know is that for decades, a vault in the heart of India held billions of dollars worth of international monetary gold, a forgotten outpost of the global financial system, far from the famous vaults of New York and London.

In an era of increasing interest in gold reserves, central bank transparency, and the potential return of gold to a more prominent monetary role, the Nagpur story deserves to be remembered.

This article was compiled through analysis of primary IMF archival documents, annual reports from 1947-1955, and specialist research on central bank gold holdings. The author welcomes corrections and additional source material from readers with access to IMF archives or Reserve Bank of India historical records.

All rights reserved ©2026 Decimal Point Analytics Pvt. Ltd.